Figure AI has been producing one humanoid robot per hour at its San José, California facility since April 2026. That is a 24-fold increase over four months. In China, Unitree Robotics plans to build 20,000 units in 2026, four times the prior year figure. Tesla has announced it will begin serial production of its Optimus robot by late summer. What was a laboratory promise for decades now has a production schedule.

BotQ: A Factory That Scales Itself

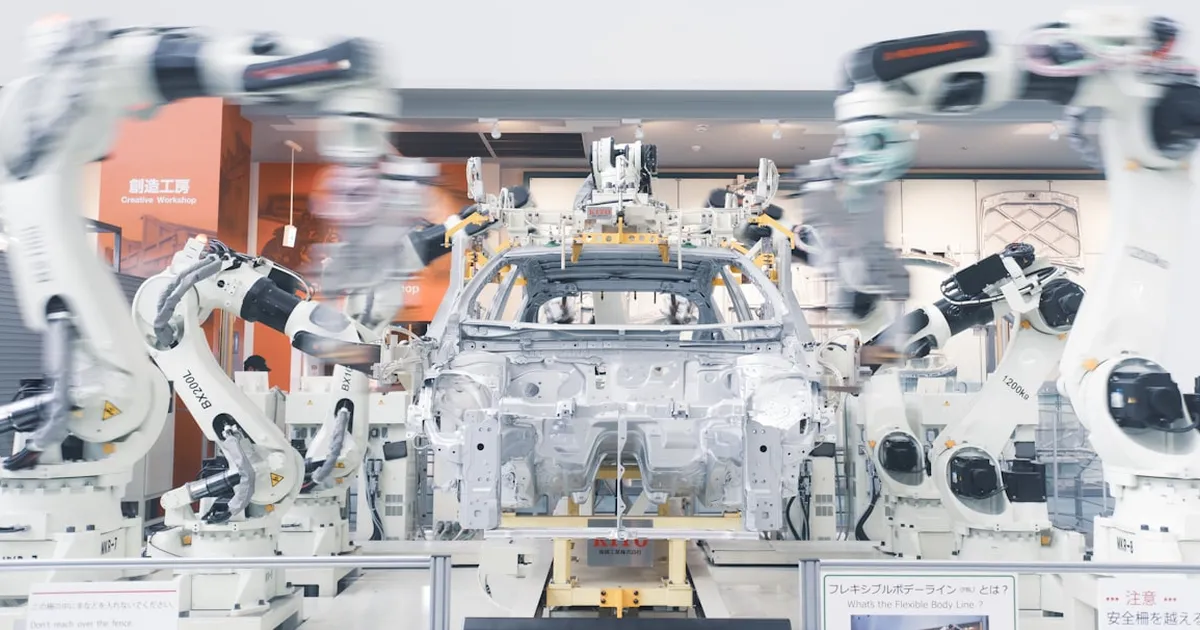

The facility is called BotQ and serves as Figure AI's pilot plant for scaling. In January 2026, a robot rolled off the line every few days. By April, the rate reached about 55 units per week, one per hour. The first-pass yield, meaning the share of robots passing initial quality checks without rework, stands above 80 percent according to Interesting Engineering. That is a strong result for a new production line: typical automotive factories start below 70 percent and take years to reach 90.

Figure AI has delivered more than 350 robots to date. Customers include BMW plants in Leipzig, Germany and Spartanburg, South Carolina, where the machines handle repetitive tasks in body shop production, such as inserting trim panels. The Figure 03 costs around 30,000 dollars per unit, roughly a year's wages for an industrial worker in many countries and, in principle, within reach for mid-size manufacturers.

China's Lead: Over 80 Percent of Global Shipments

Around 90 companies worldwide are now developing humanoid robots, up from about 55 a year ago. China accounted for more than 80 percent of all units shipped in 2025. Unitree Robotics and Agibot together held 81 percent of global shipments, according to market analysts cited by Yahoo Finance. Unitree's H2 model is priced at around 30,000 dollars, directly competing with Figure on price. The difference lies in scale: Unitree plans 20,000 units for 2026; Figure has built annual capacity of roughly 12,000.

Who sets the pace in this market has strategic significance well beyond factory floors. Humanoid robots capable of general-purpose tasks in ordinary production halls could fundamentally change manufacturing automation. Conventional industrial robots are programmed for single movement sequences and fixed in place. A humanoid robot can be redeployed to a different hall, a different task, and run on updated software. It is the first universally deployable manufacturing assistant without a fixed physical interface.

Tesla, BMW, and the First Wave of Commercial Deployment

Tesla plans to start serial production of its Optimus robot at its Fremont factory by late July 2026. The company has stated a long-term target of one million units per year. For 2026, internal targets of around 50,000 units have been reported by industry media, though whether Tesla will meet this figure is uncertain: the company has shifted production timelines repeatedly in the past. Confirmed is that Optimus will first be deployed inside Tesla's own plants as a commercial test case before external orders are accepted.

BMW Leipzig was among the first automotive plants to run humanoid robots in a pilot program, in cooperation with Figure AI since 2024. The robots take on tasks that are physically demanding and highly repetitive, exactly the work associated with the highest human absenteeism rates.

Pilots in 2026, Large Orders in 2027

Industry forecasters, including market research service TIMEWELL, see 2026 as the year of pilots and first deliveries, and 2027 as the year of the first industrial large-scale orders. By then, manufacturers must demonstrate their machines can operate reliably not just under controlled conditions but over months in normal production environments with dust, noise, changing temperatures, and unexpected situations. Conventional industrial robots went through years of validation cycles before reaching this bar.

The broader question is whether the technology matures fast enough to meet the ambitious shipment targets. Mass production of humanoid robots follows different economics than traditional special-purpose machinery: it requires scale effects, low-cost components, and short iteration cycles. That dynamic currently favors the Chinese manufacturers who hold most of the market, and analysts expect that structural advantage to persist at least through the first phase of commercial deployment.